Revisiting the Interaction between the Nigerian Residential Property Market and the MacroeconomyIsmail OJETUNDE, Nigeria

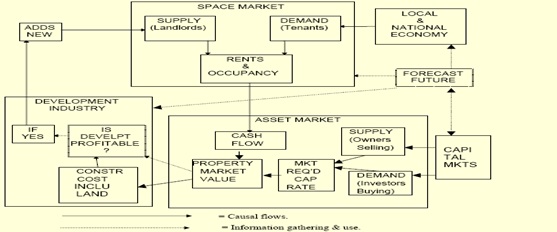

1) This paper is a Nigerian Peer Review paper, which was presented at FIG Working Week 2013, 6-10 May, in Abuja, Nigeria. Like last month article, this paper highlights one of the challenges Nigerian surveyors are dealing with, namely the Nigerian property market. At the conference many papers highlighted the current challenges Nigerians surveyors are faced with. You can find the papers here. Key words: Macroeconomy, property, property market, residential, rents. SUMMARYThe study of residential price dynamics and macro economic developments are important for virile economic and social policies formulation at both local and national scales. This paper revisits the interaction between the Nigerian macroeconomy and the operation of its residential property market using econometric analysis. By employing a larger sample and different data analysis approaches (pairwise correlations, cointegration, granger causality and vector autoregression) the objective is to provide further evidence on the extent to which the property market is integrated or linked to macroeconomy. Evidence suggests that macroeconomic variables (real gross domestic product, inflation, exchange and interest rates) have long term relationship with residential property rents in Nigeria. The results of the granger causality shows that both exchange and interest rates have useful information for predicting residential property rents over and above the past values of other macroeconomic variables. Aside, the result of the variance decomposition within the vector autoregressive model further confirmed that real GDP and Exchange rate combined forecast 31.4% of the variance in residential property rents. This study concludes that the response of the residential property market to macroeconomic shocks of interest rate, real GDP, and exchange rate implies a relatively slow adjustment of the property market to the ever changing macroeconomic events in Nigeria making long run equilibrium elusive. These findings are significant for the continued development of the Nigerian property market which is fraught with poor market information. 1. INTRODUCTION Residential property is a dynamic commodity characterized by structural durability, spatial immobility and its physically modifiable nature. As a consumption and investment commodity, residential property exerts profound influence on the socio-economic and psychological well-being of individuals, households and socio-ethnic groups. Since residential property constitutes the bulk of any country’s tangible capital, the study of residential price dynamics and macro economic developments are important for economic and social policies formulation on both local and national scales. Numerous theoretical and econometric studies have however investigated the relationship between residential price (which has remained a significant feature of most markets for housing services in the world) and the economy (for example, see Barras and Ferguson, 1985, 1987a & 1987b; Hekman, 1985; Kling and McCue, 1987& 1991; DiPasquale and Wheaton, 1996). Aside investigating the link between property and the wider economy, a point of convergence in these previous literature, is the existence of interaction and interdependency between property and the economy. For instance, during periods of macroeconomic stability, cycles in property tend to be endogenous (caused by disequilibria in the sector) and are relatively subdued and in periods of macroeconomic instability, property cycles tend to be exogenous (caused by various conditions in the macroeconomy) and sometimes feature exceptional fluctuations (Dehesh and Pugh, 1995 p.2581). Although this cause and feedback mechanisms described by Dehesh and Pugh (1995)is a feature of most market based system, the focal point of this research however is not on endogenous influences, but rather the nexus between real estate and exogenous influences of the economy. Earlier studies of this nature provided evidence on the link between property and the exogenous factors of the economy but have been considerably skewed to only the United kingdom and United States (McCue and Kling, 1994; Brooks and Tsolasco, 1999; Ling and Naranjo, 2003) with both countries having well integrated and transparent property markets. In developing countries, such evidence is limited to India (Joshi, 2006; Vishwakarma and French, 2010). In Nigeria, recent study by Ojetunde et al. (2011) has empirically discountenance the assumption that the residential property market in Nigeria is not coupled or linked with the economy. This research revisit the interaction between the economy and the operation of the residential property market by extending the study period (between 1984 and 2011) and improving on the data analysis approaches in Ojetunde et al. (2011) study. Unlike studies in developed economies which employed data on paper-backed securities, this study explore the use of nominal rents from direct property investment in the absence of property returns from the Nigerian Stock Market. 2. THE OPERATION OF THE RESIDENTIAL PROPERTY MARKET AND THE ECONOMY: A REVIEW Unlike other highly durable goods, the market for property and by extension, the operation of residential property presents a somewhat peculiar complexity as it comprises three (3) independent but connected markets linked to the economy. Fig.1 provides for a simple residential property model and link it with other exogenous systems (local and national economies and the capital markets). To start with, the model shows three important components (space, asset and development markets) which on their own represent market arenas where trade take place and prices are determined through demand and supply interplay ( Keogh 1994; Fischer 1999 and Geltner et al., 2007). The space market involves the interaction of the demand by residential property users with the current stock of space made available by the landlords. It is this result of demand-supply interaction which predicts the pattern of rents and the level of occupancy with vacancy clearing the market. Within the space market, the demand for residential space is aptly affected by the national and local economies. A growth in real wages for example may encourage new households’ formation and hence an increase in demand for residential physical space. For instance, property rights can be packaged in the short run in form of use rights to property users in return for residential rents (use values). In the asset market, Viezer, (1999) concludes that the rent determined in the space market is central in determining the demand for real estate assets because this cash flow in form of rents interacts with the cap rates required by investors, with the end product being the property market/ capital values.

As such what investors are really buying is the discounted present

value of asset’s expected income flow. The cap rates which investors

require in sealing real estate transactions in the asset market are

affected by opportunity cost of capital (since the desirability of

buying and selling real estate must be considered within a wide spectrum

of other investment opportunities operating within the capital markets),

growth expectation of future rents and investors perception of risk

associated with real estate investment vis-à-vis other investment

outlets in the capital markets (Ling and Archer, 1997b and Geltner et

al., 2007). On one hand, clear independency however exists between space (use) and asset markets with respect to right to use space (user rights) as different from the right to hold a purely financial investment interest in property (investor rights). On the other hand, connectivity is evident as the use and investment rights subsisting in a property ownership (for instance in an unencumbered freehold interest) is mediated through the development market to meet changing market requirements of users and investors. It is these market changes in users and investors requirements which stimulate development activity and development in turns supplies new user and investors rights into the market (Keogh, 1994). For example, development would only occur insofar as property rent can offset the long run marginal cost of a property (Geltner et al., 2007). It is this singular condition which ensures that the development market employ physical and financial resources to construct new built space as well as refurbishment, rehabilitation or conversion of existing buildings. The role of development therefore comes to bear in differing ways: An economy in recession needs existing built space so as to continue to function. Conversely, structural changes in form of modifying existing dwellings (through refurbishment and conversion) and new construction of dwellings (resulting from outward expansion on undeveloped land) is necessary due to economic growth or structural shifts in the economy. Aside the foregoing simple property market model, numerous empirical studies by Barras, (1983); Barras and Ferguson, (1987a, 1987b) and Barras, (1994) have shown how building boom is triggered through the combinations of conditions in the real economy, credit economy and property market. The focal point of these studies is the derivation of a theoretical framework which has been tested using time-series modelling techniques to uncover the dynamics and operations within the property market. Exploring this theme with minor variant, Dehesh and Pugh (1995, p.2583) have also show considerable evidence that cycles in property has deep cause-consequence interdependency on the financial and credit cycles even at a global scale. They further argue that such structural change resulting from changes in the financial sector requirements may occur contemporaneously with and interact with the fluctuations in both the macroeconomy and the credit markets, thereby heightening inflation, causing financial collapse and leading to recession in the property sectors. Previous studies linking property to the economy over time, however, fall principally into two distinct categories: those that centre explicitly on property- backed securities such as real estate investment trusts (Hartzell et al., 1987; Chan et al., 1990; McCue and Kling, 1994; Brooks and Tsolacos, 1999; Ling and Naranjo, 1997; Ling and Naranjo, 2003) as against those on direct property market variables, as diverse as construction series and rents ( Kling and McCue, 1987 ; Kling and McCue, 1991 ; Giussani, et al., 1992). Table 1 summarizes previous empirical research linking property with the economy. These empirical investigations are preponderant in the USA with most employing vector autoregressive framework as their methodology and few using regression analysis. Within the first category, Chan et al. (1990) for instance examine the connection between some pre-specified macroeconomic variables and real estate returns from the stock market using regression analysis. They find that changes in risk, unexpected inflation and term structure are significant predictors; while changes in industrial production and expected inflation have no significant influence on real estate returns. McCue and Kling (1994) however extend the examination of the link between property and the economy in another direction. They treat real estate returns as a residual by controlling for the covariance between equity REIT returns and the overall stock market resulting from industry effects. In their analysis, the authors employ vector autoregressive model to test the relationships between this real estate residual and macroeconomic variables and conclude that macroeconomic variables account for 60% variance in real estate returns. Brooks and Tsolacos (1999) take a similar approach to McCue and Kling (1994) study by also removing the impact of the general stock market on equity REIT series but using UK dataset. They suggest that unexpected inflation and term structure have a contemporaneous rather than a lagged effect on property returns. The absence of lagged effect however implies that changes in unexpected inflation and term structure are quickly incorporated into property returns. The authors further contend that property returns are explained by own lagged values: current property returns may have predictive power for future property returns. They hypothesise that this own lagged effect is partly due to the fact that property returns may reflect property market influences (rents, yield and vacancy rates) rather than macroeconomic variables and partly because macroeconomic and property data are not in a direct measurable form. A departure from the above categorization is the studies by Kling and McCue (1987) and Kling and McCue (1991) who focus on property market indicator. They advocate the use of construction series from direct real estate investment and employ vector autoregressions to model industrial and office construction cycles. They find that macroeconomic variables influence real estate series indirectly through other macroeconomic variables. The authors also show that adjustment to macroeconomic shocks take place with a lag, resulting from the existence of long production period between new construction starts and completions. Giussani et al. (1992) also examine the relationship between changes in commercial rental values and fluctuations in economy activity using a predictive model. They analyse monthly data from 1983 to 1991 from Europe and find that real Gross Domestic Product (GDP) is the most significant explanatory variable for rental values. This result is consistent with those reported in Hetherington (1988) and Keogh (1994) that GDP is a determinant of rents, to the extent that rents are closely correlated with the business cycle. Table 1. Classification of Studies Linking Property with the Economy.

By using non- food credit as proxy for housing price in India, Joshi (2006) employs a structural vector autoregressive model for the period 2001 to 2005 and asserts that both credit growth and interest rate influence the housing market and stabilize other sectors of the economy. Vishwakarim and French (2010) also examine the influence of macroeconomic variables on the India real estate sector between 1996 and 2007. Using a structural break, they conclude that macro economic variables explain 10% of the variation in the real estate market between 1996 and 2000 with such variation increasing to 23% between 2000 and 2007. In Nigeria, Ojetunde et al. (2011) estimated a vector autoregressive model and suggest that macroeconomic shocks explain 28% of the variation in residential property rents. They further hypothesized that, responses of residential property rents to shocks in real GDP, exchange rates and short-term interest rates reflect the fact that rents from direct residential property and by extension, the market for residential property adjust slowly to changes in macroeconomic events. Their study however did not establish the presence of long run equilibrium between the Nigerian macroeconomy and its property market. This is one of the focal point of this research. 3. THE DATA The data were extracted from two distinct sources namely: the registered Estate Surveying and Valuation firms and the National Bureau of Statistics (NBS). The aggregation of residential rental price data was supplied by registered estate surveying and valuationfirms based on available letting evidence in most parts of Nigeria. National economic data as varied as Gross Domestic Product (GDP) in real terms, short-term interest rates, inflation and exchange rateswere provided by National Bureau of Statistics (NBS). Theirinclusion in the final analysis was premised on the assumption that trend in real estate returns is correlated with happenings within the real and credit economy. The sampledata in annual frequency covers the period 1984 to 2011 with a total of 28 observations. Table 2 reportsa summary of the descriptive statistics of the data sample. Table 2. Summary of Descriptive Statistics of Variables.

4. METHODOLOGY The methodology consists of four different approaches: pairwise correlation between the variables, Cointegration test, Granger causality tests(block exogeneity wald tests), and Vector autoregression (VAR). Cointegration and granger causality tests are within the vector autoregression framework employed in this research. The pairwise correlation examines the correlation between the residential rent and marco economic variables. A vector autoregressive (VAR) framework was employed for the period 1984 to 2011 in order to investigate the relationship between residential property market (using RESDRENT as proxy) and macroeconomic variables (INFLATN, EXCHAG, INTEREST, GDP). A vector autoregressive model is a systems regression model in which the variance or current values of the dependent variables can be explained in terms of the different combinations of their own lagged values and the lagged values of other variables as well as their uncorrelated error terms. The reduced form of the estimated VAR model is expressed as: Table3. VAR Lag Order Selection Criteria

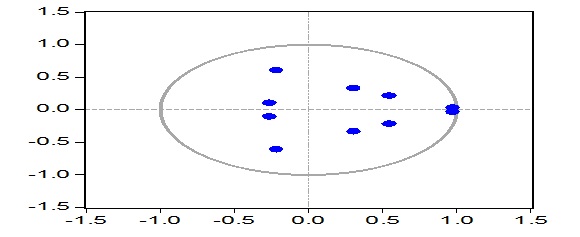

*indicates lag order selection by criterion. Where LR denotes: sequential modified LR test statistic (each test at 5%level); FPE: Final prediction error; AIC: Akaike information criterion; SC: Schwarz information criterion and HQ: Hannan-Quinn information criterion. While LogL is thelog likelihood function. Analysis of this magnitude presumes the presence of stationary within the data series(Brooks, 2008).The examination of the inverse roots of the autoregressive polynomial (fig.2)however reveals that the absence of non- stationary in all VAR variables, since none of the roots has a modulus greater than one and none lies outside the unit circle.

Johansen (1988)

cointegration test is applied to the VAR variables to test the

assumption that the five variables are bound by some long run phenomena,

though the variables might deviate from their short run relationship.

The trace and max tests for cointegration under the Johansen approach

show whether the null hypothesis of no cointegration vectors should be

rejected. The estimated variance decomposition of RESDRENT, is the proportion

of the variance in RESDRENT that can be explained by its own shocks and

shocks to other variables. The forecast error variance (S.E) for an four

(4) period forecast horizon within the estimated variance decomposition

determines the proportion of RESDRENT for current and future periods (1,

2,3 and 4) which is accounted for by innovations to INFLATN, EXCHAG,

INTEREST and GDP. It is expected that the total percentage of the

forecast variance due to all innovations for each period sum up to 100.

Impulse response function (IRF) is further generated for the estimated

coefficients matrices in VAR model. The impulse response function traces

out the response of RESDRENT in the VAR system to shocks in the error

terms 5. RESULTS The pairwise correlations in Table 4 show two important results.

First,residential property rents are strongly and positively correlated

with real GDP and exchange rates fluctuations in Nigeria. Secondly,

there are negative but weak correlations between residential property

rents and short–term interest rates as well as between residential

property rents and inflation rates. These results though a working

hypothesis, are later confirmed in the Variance decomposition within the

VAR framework later in this section.

The Johansen cointegration test in Table 5shows the eigen value, statistic, critical value and probability value at 5% level of significance. By examining the trace test within the first two panels of the table, null hypothesis of four cointegrating vectors at 5% level is rejected as the trace statistics are greater than the critical values. The max test shown in the other panel confirms this result. On the basis of the granger causality test, it can be seen that with the exception of inflation other macro economic variables forecast RESDRENT. In this case all the lag coefficients of each of the macroeconomic variables are statistically significant (p-values are less than 5%) in the residential property rent equation, as indicated in the last panel of table 6. As a corollary, granger causality tests also show that while both the

short -term interest rates and exchange rates have significant effects

in the residential property rents, there is evidently ‘no reverse

significant’ of residential property rents on these two macroeconomic

variables ( their P Value are 0.2677 and 0.2838 respectively). These

results suggest that these two macroeconomic variables (short-term

interest rate and exchange rate) ‘granger cause’ residential property

rents and that these two macroeconomic variables have useful information

for predicting residential property rents over and above the past values

of other macroeconomic variables in the VAR model.

Table 6: Granger Causality/ Block Exegeneity Wald Tests

Again, residential property rents and real GDP which are both significant imply the existence of feedback relationship between real GDP and residential property rents. The variance decomposition of residential rents to shocks or innovations in macroeconomic variables in Table 7 further confirms this result as it shows the contribution of each macroeconomic shock to residential property rents. Table 7: Variance Decompositions for Residential Property Rent

Cholesky ordering: RESDRENT INFLATN EXCHAG INTEREST GDP. The forecast error variance (S.E) for four (4) years shows that real

GPD and Exchange ratetogether forecast 31.4% of the variance in

residential property rents. This result is consistent with those

reported in earlier studies byKeogh (1994) that GDP predicts the pattern

of rents and the findings of McCue and Kling, (1987); Kling and McCue,

(1994) that short- term interest rates contributes to the variation in

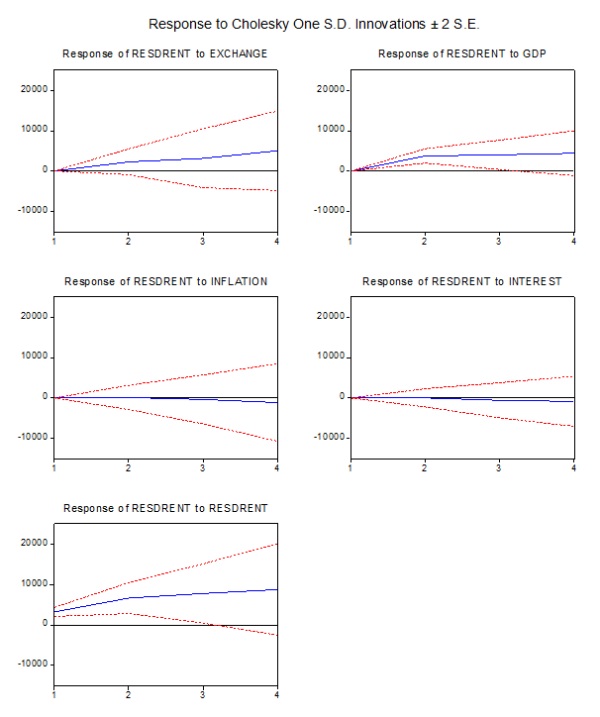

property returns performance. Finally, the Impulse Response Function

(IRF) as depicted in fig. 3shows that shocks to short-term interest

rates have a negative significant impact on residential property rents,

with the shocks getting a bit pronounced afterperiod two. Shocks or

innovations in inflation is negative but not significant and the shocks

die away instantly even at year zero. Increase in real GDP and exchange

rates have significant positive effects on residential rents. In this

case, rents appear to settle down quickly to a steady rising state after

period onedue to shocks of exchange rate and in the second period year

to shocks of real GDP. 6. CONCLUSIONS Revisiting the interaction between the Nigerian property market and the macroeconomy has further confirmed that the use of econometric analysis rather adhoc methodologies purged with simple trend interpolations is plausible. Since residential property rent is a significant feature of most property market in the world, empirical evidence based on this study from Nigeria implies that exogenous influences of the economy (real GDP and Exchange rate) account for 31.4% of the variation within the residential property market. At a disaggregate level, real GDP accounts for a substantial proportion (17.3%) of this variation in the residential property market, while exchange rate account for the remaining 14.1% of these residential property market variance. In addition the feedback mechanism between GDP and residential property rents, means that these two variables are determined contemporaneously and by implication depicts a somewhat limited integration of the Nigerian residential property market with the economy. The one to two period(s) response shocks of interest rate, real GDP, and exchange rate show a relatively slow adjustment of the market to the ever changing macroeconomic events in Nigeria. Such responses are exogenous and make long run equilibrium within the residential property market almost elusive. The existence of such analysis of this nature will in the end aid useful property market analysis in a market fraught with poor property market data.

Fig.3. Responses of Residential Property Rent to Shocks in MacroeconomicVariables. REFERENCES Barras, R. (1983). A simple theoretical model of the office

development cycle. Environment and Planning A, 15, pp.1381-1394. CONTACT Ismail Ojetunde

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||